The Complete Guide to the Arizona Pre-Qualification Form

What every buyer, listing agent, and seller should know before they trust a pre-qualification letter — explained line by line by a 24-year West Valley mortgage broker.

By Joe Hansen, NMLS# 217716 · Precision Mortgage, Peoria AZ · Serving Peoria, Glendale, Surprise, Goodyear, Buckeye, Avondale, Litchfield Park, El Mirage, Sun City, Sun City West & Phoenix

In 24 years of originating mortgages across the West Valley, I have signed more Arizona Association of REALTORS® Pre-Qualification Forms than I can count. It’s one of the most common documents in any Arizona real estate transaction — and one of the most misunderstood. Buyers assume it’s a guarantee. Agents sometimes treat it as a formality to attach to an offer. Sellers occasionally discover, weeks into escrow, that the form they relied on was based on far less verification than they assumed.

The form itself is short — a single page with around 40 numbered lines. But what stands behind those lines can vary enormously from one lender to the next. Two Arizona Pre-Qualification Forms can look identical, checked boxes and all, and still represent two completely different levels of confidence. One may be built on verified pay stubs, tax returns, bank statements, and a full credit pull. The other may be built on a five-minute phone call.

This guide walks through the form line by line — what each section means, why it exists, and what separates a pre-qualification that holds up under contract from one that creates problems three weeks into escrow.

What the Arizona Pre-Qualification Form Actually Is

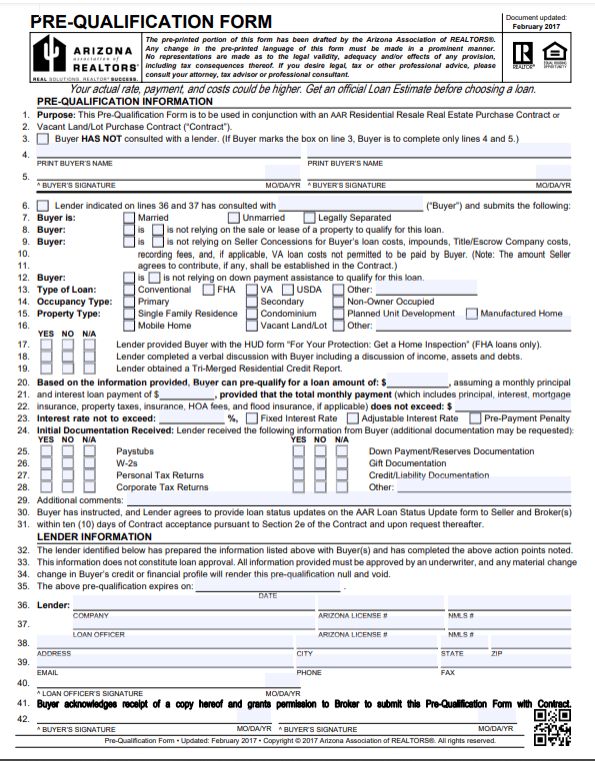

The Pre-Qualification Form is drafted and copyrighted by the Arizona Association of REALTORS® and is designed to be submitted alongside an AAR Residential Resale Real Estate Purchase Contract or Vacant Land/Lot Purchase Contract. It’s completed and signed by the buyer’s lender — not by the buyer or the real estate agent — and its purpose is narrow but important: to give the seller and listing agent a documented snapshot of the buyer’s ability to obtain financing at the time the offer is submitted.

It is not a loan approval. The form says so directly. A lender preparing this form has completed the listed action points, but this information does not constitute loan approval — all information must still be approved by an underwriter, and any material change in the buyer’s credit or financial profile can render the pre-qualification void. That single sentence is the most important on the entire form, and we’ll come back to it.

What the form does do is create a paper trail. It documents what the buyer told the lender, what the lender verified, what loan program is being pursued, and what financial limits the offer is built around. In a competitive West Valley market, that paper trail is often the difference between an offer a seller trusts and one they pass over for a stronger-looking buyer.

Walking Through the Form, Line by Line

The Arizona Pre-Qualification Form is numbered top to bottom, and once you know what each line actually asks, it stops being a mystery and starts being a useful tool. Here’s exactly what’s happening at the lines that matter most — the ones that determine whether your offer reads as strong or weak to a seller and listing agent.

Lines 8–9: Marital Status and Reliance on the Sale of Another Property

LINES 8–9

Lines 8 and 9 ask two foundational questions: is the buyer married, unmarried, or legally separated, and is the buyer relying on the sale or lease of another property to qualify for this loan.

The marital status question matters more in Arizona than in many other states, because Arizona is a community property state. That single fact affects how a married buyer’s debts and assets get treated in underwriting, how title can be held, and in some cases whose income and credit profile gets pulled into the file even if only one spouse is on the loan. It’s not a throwaway question — it’s foundational to how the rest of the file gets built.

The “relying on the sale or lease of another property” question is just as important, and it’s one sellers should read carefully. If a buyer in Peoria needs to sell their current home before they can close on a new purchase in Surprise, that’s a real contingency baked into the deal — not a detail to discover three weeks into escrow when the buyer’s current home hasn’t sold yet. A clean “no” on line 9 tells a seller the buyer’s financing doesn’t depend on a second transaction closing first. A “yes” means there’s a second moving part the seller needs to factor into how competitive — and how risky — the offer really is.

Lines 12–15: Seller Concessions

LINES 12–15

Lines 12 through 15 cover whether the buyer is or is not relying on Seller Concessions for the buyer’s loan costs — prepaid items, impounds (the reserve account for taxes and insurance), Title/Escrow Company costs, recording fees, and, where applicable, the specific VA loan costs that veterans are not permitted to pay themselves under VA guidelines. The form is explicit that the actual dollar amount the seller agrees to contribute, if any, gets established separately in the purchase contract itself — this section of the Pre-Qualification Form simply flags whether concessions are part of the plan at all.

Why this matters in today’s market: Seller concessions can make or break a deal’s competitiveness. In a market where multiple offers are still common on well-priced West Valley homes, an offer asking the seller to credit several thousand dollars toward closing costs is, functionally, a lower net offer — even if the purchase price looks identical to a competing offer with no concessions requested. Sellers and listing agents read these lines closely, because they tell them what they’re actually netting at closing.

That said, concessions aren’t a weakness by default. They’re a tool. A buyer who is light on cash but strong on income and credit can use a seller credit to buy down their rate or cover costs, making a 6.5% rate feel more like 5.75% for a year or two through a temporary buydown, or simply preserving cash reserves for after closing. The key is structuring the offer so the purchase price plus the requested concession still reads as competitive — exactly the kind of strategy conversation I have with buyers and their agents before we submit a number.

Lines 17–19: Marital Status and Sale Reliance, Restated

LINES 17–19

In the 2017 version of the form, lines 17 through 19 restate and formalize the marital status and sale-reliance questions introduced earlier — confirming whether the buyer is married, unmarried, or legally separated, and whether the buyer is or is not relying on the sale or lease of a property to qualify for this loan. The form repeats this structure because it’s foundational to everything that follows: the loan type, occupancy type, and property type sections that come immediately after all build on top of these answers.

Lines 20–21: Type of Loan — Conventional, FHA, VA, USDA, and Other

LINES 20–21

Lines 20 and 21 are where the form identifies which loan program the buyer is pursuing — Conventional, FHA, VA, USDA, or Other — and this is one of the sections sellers and listing agents pay closest attention to, fairly or not.

Conventional loans are the most flexible in terms of property type and timeline but typically require stronger credit and either a larger down payment or mortgage insurance if putting down less than 20%. For buyers with solid credit and steady income, conventional financing is usually the most straightforward path — read more on my Conventional Loans page.

FHA loans allow down payments as low as 3.5% and are more forgiving on credit history, making them a strong option for many West Valley first-time buyers. The tradeoff is mortgage insurance that, in most cases, doesn’t go away until the loan is refinanced, plus a few additional property condition requirements at appraisal. I’ve broken down how FHA financing works in Arizona, including upfront and annual mortgage insurance premiums, on my FHA Loan Arizona page.

VA loans remain, in my opinion, the single best loan program available to anyone who qualifies. Zero down payment, no monthly mortgage insurance, and competitive rates make VA financing extremely strong — particularly here given our proximity to Luke Air Force Base and the large veteran and active-duty population throughout Peoria, Glendale, and Surprise. One thing sellers sometimes misunderstand: VA appraisals carry minimum property requirements similar to FHA’s, not stricter, and a well-prepared VA offer is just as strong as any other in this market. I cover eligibility, entitlement, and the appraisal process on my VA Loan Peoria AZ page.

USDA loans offer zero down payment financing but are limited to eligible rural and suburban areas, which rules out most of the core West Valley but can apply to certain outlying pockets depending on current USDA maps.

Down payment assistance programs — like Home Plus Arizona or the Chenoa Fund — aren’t a separate checkbox on this line, but they layer underneath an FHA or conventional first mortgage to cover some or all of the down payment. These are excellent tools for buyers with strong income and credit who haven’t had time to save a large cash reserve. The tradeoff sellers should understand: DPA-backed offers function exactly like any other FHA or conventional offer once underwritten — the difference is the income source for the down payment, not the underwriting standard.

A practical example: Say a Surprise listing gets two offers at $425,000. One is conventional with 20% down. The other is FHA with Home Plus down payment assistance and a request for $6,000 in seller concessions on lines 12–15. On paper, the second offer looks “weaker.” But if both buyers have been fully documented — income verified, credit pulled, assets confirmed — and both have realistic closing timelines, the actual performance risk may be nearly identical. The form alone won’t tell a listing agent that. The conversation behind the form will.

Lines 22–24: Occupancy Type, Property Type, and the FHA Inspection Disclosure

LINES 22–24

Lines 22 through 24 document the Occupancy Type — Primary, Secondary, or Non-Owner Occupied — and the Property Type, with options including Single Family Residence, Condominium, Planned Unit Development, Manufactured Home, Mobile Home, Vacant Land/Lot, or Other. This isn’t a minor checkbox. Loan programs, rates, and down payment requirements differ meaningfully between an owner-occupied purchase and an investment purchase, and condominiums in particular can require additional approval steps depending on the lender and the HOA’s financials. A pre-qualification that doesn’t match the actual occupancy intent isn’t worth much, and I’ve seen offers get held up simply because the occupancy box didn’t match what the buyer actually told their agent.

These lines also cover, for FHA transactions specifically, whether the lender provided the buyer with the HUD-required disclosure titled “For Your Protection: Get a Home Inspection” — a consumer protection requirement reminding FHA buyers that the appraisal is not a substitute for an independent home inspection. It’s a small line, but a meaningful reminder that an appraisal protects the lender’s collateral position; it does not protect the buyer’s interest in knowing the true condition of the home.

Lines 25–28: The Most Important Section on the Entire Form

Now we get to the four lines that, more than anything else on this document, determine whether a pre-qualification letter means something or means almost nothing.

Line 25: The Verbal Discussion Question

Line 25 confirms whether the lender completed a verbal discussion with the buyer, including a discussion of income, assets, and debts. It’s phrased simply. It’s a single checkbox. And it is, without exaggeration, the line that separates a real pre-qualification from a guess with a letterhead.

Here’s why this matters so much: the form only requires a verbal discussion to be checked off. It does not, by itself, require the lender to have looked at a single document. Two lenders can check that same box under completely different circumstances. One lender spent fifteen minutes asking a buyer their income, their job, their approximate debts, and their estimated credit score — took their word for all of it — and issued a pre-qualification letter. Another lender pulled actual pay stubs, ran the numbers against two years of tax returns, reviewed real bank statements, and pulled a full tri-merged credit report before signing anything.

Both letters can look identical to a listing agent. Both check the same box on line 25. But only one of them reflects work that has actually been verified.

This is the gap I built my entire pre-qualification process around closing. When I prepare a pre-qualification for a buyer — regardless of whether they’re buying in Peoria, Sun City, Buckeye, or anywhere else in the West Valley — I do not rely on a verbal conversation alone if I can avoid it. Whenever possible, before I sign anything, I review actual pay stubs covering the most recent 30 days to confirm gross income and consistency with what was reported; W-2s for the past two years to verify employer history; tax returns, especially critical for self-employed borrowers, commission-based earners, or anyone with rental income or significant deductions; bank statements covering the last two months to confirm funds exist and large deposits can be sourced; retirement account statements when 401(k) or IRA funds are part of the down payment or reserves; gift fund documentation, including the gift letter and proof the funds actually moved from the donor’s account; self-employed income documentation, including profit-and-loss statements and business tax returns; and a buyer’s employment history, since unexplained gaps or recent job changes can affect both qualification and loan program eligibility.

When all of that has actually been reviewed — not just discussed, but reviewed — line 25 means something completely different than it does on a verbal-only file. It means the income is real and matches what’s claimed. It means the assets exist and can be sourced. It means there isn’t a self-employment tax return sitting out there with a number the buyer didn’t realize would affect their qualifying income. It means far fewer surprises are waiting in the underwriting file three weeks after the offer was accepted.

This is also exactly why I tell every buyer and every agent I work with the same thing: ask the lender directly whether they reviewed actual documents, or whether line 25 is checked based solely on what the buyer told them over the phone. It’s a fair question, and a transparent lender will answer it honestly. If you’re a buyer reading this before you’ve gotten pre-qualified anywhere, I’d encourage you to start with a real review rather than a phone call — see exactly what that process looks like on my Mortgage Pre-Approval page.

Line 26: The Tri-Merged Residential Credit Report

Immediately below the verbal discussion line, line 26 asks whether the lender obtained a Tri-Merged Residential Credit Report. This line gets far less attention than it deserves.

A tri-merged credit report pulls data from all three major credit bureaus — Experian, Equifax, and TransUnion — and merges it into a single report mortgage lenders use to evaluate a borrower. This is different from the free credit score apps or single-bureau scores buyers often check on their phone. Mortgage scoring models, and the tri-merge report itself, can show meaningfully different numbers than a consumer credit app — sometimes by 20, 30, even 50+ points in either direction.

Why does line 26 matter so much for a pre-qualification? Because nearly everything downstream depends on accurate credit data. Credit score determines loan program eligibility, interest rate, and in some cases the minimum down payment required. Debt-to-income ratio (DTI) — the relationship between a buyer’s monthly debt obligations and their gross monthly income — is one of the single biggest factors in how much a buyer actually qualifies to borrow, and it can only be calculated accurately once every monthly obligation is known, since car payments, credit cards, personal loans, and other mortgages all factor directly into that calculation, and buyers often forget an obligation or two when simply asked over the phone. Collections accounts can affect both credit score and, depending on the loan program and size of the collection, may need to be addressed before clear-to-close. And student loans are a particular trap in verbal-only pre-qualifications, because many buyers don’t realize their payment is calculated differently than they assume — some programs use the actual reported payment, others use a percentage of the balance if the loan is in deferment or income-based repayment, and that difference alone can shift a buyer’s qualifying picture meaningfully.

A pre-qualification based on a buyer’s self-reported credit score and self-reported debts is, frankly, a guess dressed up as a number. A pre-qualification built on an actual tri-merged credit pull on line 26 is a real assessment. I pull credit on every pre-qualification I issue whenever circumstances allow it, specifically because I’d rather catch a DTI issue or a forgotten collection account before a buyer writes an offer — not after they’re already three weeks into a 30-day escrow.

Lines 27–28: The Pre-Qualified Loan Amount and Initial Documentation Received

Lines 27 and 28 are where the lender states the actual numbers: the loan amount the buyer can pre-qualify for, the assumed monthly principal and interest payment, and the maximum total monthly payment — covering principal, interest, mortgage insurance, property taxes, insurance, HOA fees, and flood insurance where applicable. This is immediately followed by the Initial Documentation Received checklist, where the lender confirms what’s actually been collected from the buyer so far — pay stubs, W-2s, tax returns, bank statements, and similar items — with a note that additional documentation may still be requested as the file moves forward.

This is the section where the difference between a documentation-based pre-qualification and a verbal one becomes most visible on paper. If those boxes are checked, it’s worth asking what was actually reviewed behind them — not just whether a document was received, but whether it was reviewed against the income and asset figures the buyer reported on lines 25 and 26. Receiving a document and analyzing it are two different things, and only one of them actually de-risks the file.

Line 35: Loan Status Updates and the Expiration Clock

LINE 35

Line 35 falls within the section of the form that commits the lender to providing Loan Status Updates to the seller and the brokers involved — typically within five to ten days of contract acceptance, depending on the form revision in use, and again upon request thereafter. This is done using the companion AAR Loan Status Update form, and it exists specifically so sellers aren’t left wondering about financing progress during escrow. A responsive lender treats these updates as routine; a buyer working with an unresponsive lender often finds out the hard way that updates aren’t coming on time, which creates unnecessary anxiety for everyone in the transaction.

This same closing section of the form also establishes the pre-qualification’s validity period — typically tied to the buyer’s authorization and the underlying credit pull, since credit reports and verified income documentation have a shelf life. A pre-qualification issued three months ago, based on data that’s three months stale, isn’t something a seller should weigh the same as one issued last week.

One detail worth repeating from the form itself, because it’s the most legally important sentence on the page: any material change in the buyer’s financial situation between the date of this form and closing can void the pre-qualification entirely. A new car loan, a job change, a large credit card purchase, a missed payment — any of these can alter the picture enough that the original pre-qualification no longer reflects reality. This is exactly why I tell every buyer the same thing the moment we go under contract: don’t open new credit, don’t change jobs, don’t make any large purchases until we’ve closed. It sounds obvious until it isn’t — I’ve seen buyers lose financing over a new furniture purchase made “on the store’s 12-months-no-interest plan” two weeks before closing.

Basic Pre-Qualification vs. Documentation-Based Pre-Qualification

This is the core of what separates a pre-qualification that protects everyone in a transaction from one that creates risk. The form looks the same either way. The confidence behind it does not.

| Basic, Verbal-Only Pre-Qualification | Documentation-Based Pre-Qualification |

|---|---|

| Phone conversation about approximate income, debts, and down payment | Full review of recent pay stubs and W-2s to confirm actual income |

| Self-reported credit score, not a pulled report | Full tri-merged credit report reviewed for score, DTI, collections, and obligations |

| No review of pay stubs, tax returns, or bank statements | Tax returns reviewed where self-employment, commission, or rental income applies |

| Pre-qualification amount based on estimates | Bank statements and gift funds verified and sourced |

| Risk surfaces mid-escrow, after the offer is accepted | Pre-qualification amount built on verified numbers, before the offer is written |

An offer backed by a documentation-based pre-qualification is far less likely to fall apart during the financing contingency period, because the major risks — income inconsistency, credit issues, insufficient assets — have already been identified and addressed before the offer was ever written. For buyers, it means knowing your real number before falling in love with a home you can’t actually afford, with no surprises mid-escrow about a forgotten collection account or a self-employment deduction that lowered your qualifying income more than expected.

To be clear about something equally important: no lender, including me, can guarantee final loan approval before underwriting reviews the complete file. Underwriting is the final word, and conditions can come up that a pre-qualification review didn’t anticipate. What a thorough, documentation-based review does do is dramatically reduce the odds of a major surprise, because the things most likely to derail a loan have already been caught and addressed before the buyer ever wrote an offer.

How Precision Mortgage Approaches the Arizona Pre-Qualification Form

When a buyer comes to me — whether they’re a first-time buyer in Glendale, a veteran near Luke Air Force Base, a self-employed buyer in Goodyear, or a retiree exploring Sun City — here’s what actually happens before I sign a Pre-Qualification Form. I review documentation whenever it’s available, not just discuss it — pay stubs, W-2s, tax returns, bank statements all get an actual look, not a verbal pass. I analyze the right loan program for the buyer’s actual situation, comparing conventional, FHA, VA, USDA, and down payment assistance options rather than defaulting to whichever is fastest to quote. My Loan Programs page walks through each option in more depth, and first-time buyers should take a look at my First-Time Home Buyer page, covering programs built specifically for buyers purchasing their first home in Arizona.

I discuss seller concessions strategically, not as an afterthought — if a concession makes an offer stronger by freeing up cash for a rate buydown or reserves, we structure it that way; if it makes an offer look weaker relative to the competition, we talk through the tradeoff honestly before the offer goes out. I evaluate contingencies with the buyer’s agent, making sure financing, appraisal, and inspection timelines actually match what’s realistic given the buyer’s loan program and file complexity. And I stay responsive throughout escrow, providing Loan Status Updates on time and keeping everyone informed, because silence during a financing contingency period creates anxiety that’s almost always avoidable. The result is that buyers submit stronger offers, because a verified pre-qualification gives a listing agent real reason to trust the buyer’s financing — which can matter as much as price in a multiple-offer scenario.

Already Under Contract or Wondering If Your Pre-Qual Holds Up?

If your rate or fees ever crept up after you went under contract with a different lender, or you’re wondering whether your current pre-qualification was actually built on verified numbers, I cover that exact situation in detail.Read: Switching Lenders After Signing a Purchase Contract

Common Questions Arizona Buyers Ask About the Pre-Qualification Form

Is a Pre-Qualification Form the same as a pre-approval letter?

Not exactly. The AAR form is a specific, standardized real estate document submitted with an offer, while a pre-approval letter is a broader lender document. The difference that actually matters is the same either way: was the buyer’s information verified with real documentation on lines 25–28, or just discussed verbally?

Can my pre-qualification expire before I close?

Yes. Credit reports and income documentation have a limited shelf life, which is exactly what the expiration language tied to line 35 addresses. If your home search takes longer than expected, your lender may need to refresh documentation before submitting an offer.

What happens if my finances change after the form is submitted?

Any material change — a new loan, a job change, a large purchase, a missed payment — can void the pre-qualification and create real problems with your financing contingency. Avoid new credit activity or major financial changes between contract acceptance and closing.

Do seller concessions on lines 12–15 make my offer look weaker?

They can, if not structured carefully, since sellers look at net proceeds, not just purchase price. But used strategically, concessions can strengthen a buyer’s overall position without weakening how the offer is perceived — worth discussing with your lender before you write the offer.

Why does line 26’s credit report matter more than my own credit score app?

Mortgage lenders use a tri-merged report and mortgage-specific scoring models that frequently produce different numbers than consumer credit apps. Relying on a self-reported score rather than an actual mortgage credit pull is one of the most common reasons a “pre-qualified” number turns out to be inaccurate.

The Bottom Line on Arizona’s Pre-Qualification Form

Everything that matters about this form happens off the page — in whether the lender actually reviewed pay stubs, tax returns, bank statements, and a real credit report on lines 25–28, or simply had a conversation and filled in some boxes. If you’re buying a home anywhere in Peoria, Glendale, Surprise, Goodyear, Buckeye, Avondale, Litchfield Park, El Mirage, Sun City, Sun City West, or Phoenix, I’d rather spend the time upfront reviewing your actual documentation than hand you a quick letter that doesn’t hold up under scrutiny.Start Your Documentation-Based Pre-Approval

Call or text Joe Hansen at (480) 239-7766 — let’s make sure your next pre-qualification actually means something.

“Your home. My mission. Let’s make it happen.”Joe Hansen is a licensed Mortgage Loan Officer, NMLS# 217716, AZ LO0911403, operating as a mortgage broker under Precision Mortgage in Peoria, AZ. This article is for informational and educational purposes only and does not constitute a loan commitment, pre-approval, or guarantee of financing. All loan approvals are subject to full underwriting review, credit qualification, and verification of income, assets, and other documentation. The Arizona Pre-Qualification Form referenced in this article is a copyrighted document of the Arizona Association of REALTORS® and is used in conjunction with AAR purchase contracts; this article is independent commentary and is not affiliated with or endorsed by the Arizona Association of REALTORS®. Always consult your purchase contract and a licensed real estate professional regarding specific contingencies and deadlines applicable to your transaction. Equal Housing Opportunity.