Why Your Zillow Mortgage Payment Is Wrong: The Hidden Costs Arizona Homebuyers Need to Know

You found the listing, looked at the Zillow estimate, and thought, “I can afford this.” Here’s the problem: that number is probably understating your real payment by a couple of hundred dollars a month — or more. Let’s break down exactly why. By Joe Hansen, NMLS# 217716 · Precision Mortgage, Peoria AZ · Updated 2026

I have this conversation with buyers almost every single week. They send me a Zillow listing, point to the estimated monthly payment at the bottom, and ask, “Is this accurate?” The honest answer is almost always no — and not by a small margin. Zillow’s mortgage calculator is built to give you a quick, generic estimate, not a number you should actually budget around. This post walks through exactly what it gets wrong, why it matters, and how to get a number you can actually trust. $200–$500 Typical monthly gap between Zillow’s estimate and your real payment 0.62% Average Phoenix-area property tax rate, often mis-estimated online $2,344 Average annual Arizona homeowners insurance premium

Why Zillow’s Number Looks So Different From Reality

Zillow’s mortgage calculator isn’t trying to deceive anyone — but it’s also not designed with precision in mind. It’s a marketing tool built to keep you engaged with a listing, not a financial planning tool built to give you an accurate monthly obligation. The calculator pulls a generic interest rate, applies a rough property tax percentage based on county averages, and often skips line items entirely. The result is a number that looks clean and affordable — and is frequently wrong by a couple hundred dollars a month.

As a working mortgage broker here in Peoria, I see the real numbers every day — actual rate sheets, actual county tax bills, actual insurance quotes. The gap between what online calculators show and what borrowers actually pay is one of the most common surprises I have to manage with buyers, especially first-time buyers who’ve never been through this process before. Let’s go through it question by question.

The Real Questions Arizona Buyers Are Asking

Q Does Zillow’s estimate include private mortgage insurance (PMI)?

Rarely, and almost never accurately. If you’re putting down less than 20% on a conventional loan, you’re required to carry PMI — and it isn’t a flat number. PMI rates typically range from 0.5% to 1.5% annually, depending on your credit score, your loan-to-value ratio, your debt-to-income ratio, and even the property type. A borrower with a 760+ credit score putting 10% down will pay meaningfully less PMI than a borrower with a 620 score putting 5% down — on the exact same loan amount. Zillow has no way to know your credit score, so it either omits PMI entirely or applies a generic placeholder that’s frequently wrong in one direction or the other.

Q What about FHA mortgage insurance — is that different?

Yes, and this trips up a lot of buyers. FHA loans require mortgage insurance premium (MIP) regardless of your down payment size — there’s no way to avoid it on an FHA loan, even with 20% down. FHA MIP has two parts: an upfront premium and an ongoing annual premium. Borrowers putting down less than 10% pay MIP for the life of the loan, while those putting 10% or more down can have it removed after 11 years. This is structurally different from conventional PMI, and Zillow’s calculator typically doesn’t distinguish between the two loan types at all.

Q Is the property tax estimate on Zillow accurate for Peoria and the West Valley? Often not. Property tax estimates online frequently rely on outdated assessed values or a flat statewide average rather than the actual current tax bill for that specific parcel. The Phoenix-metro average runs around 0.62% of home value annually, but the actual number depends on the specific taxing jurisdictions for that property — county, city, school district, and any special assessment districts. On a $420,000 home, even a modest miscalculation here can shift your monthly payment by $50–$100. I pull the actual tax record for any property a client is considering, not an estimate.

Q Does Zillow account for Arizona’s actual homeowners insurance costs?

Almost never with any precision. Arizona homeowners can expect to pay around $2,344 annually for homeowners insurance on average — but that figure swings significantly based on the home’s age, construction type, location, and proximity to wildfire-prone areas. Arizona is the fourth most wildfire-prone state in the country, and that risk factor is increasingly reflected in premiums, especially for homes near desert washes or undeveloped land. A generic online calculator has no way to price that in. I always recommend getting an actual insurance quote before finalizing your budget — not an assumption.

Q What about HOA fees — does Zillow include those?

Sometimes, but inconsistently, and frequently using outdated figures pulled from old listing data. HOA fees in Peoria-area communities can range from under $50 a month in older neighborhoods to $200+ a month in newer master-planned communities with extensive amenities. This is one of the easiest numbers to verify directly — but it’s also one of the most commonly wrong figures on third-party listing sites, since HOA dues change annually and aren’t always updated promptly across platforms.

Q Is the interest rate Zillow shows actually the rate I’d get?

Almost certainly not. Zillow displays a generic average rate that has nothing to do with your specific credit score, loan type, down payment, or the lender you’d actually use. Mortgage rates are priced individually based on your full financial profile. Two buyers looking at the same house, with different credit scores, can be quoted meaningfully different rates — sometimes a full percentage point apart. On a $400,000 loan, a 1% rate difference changes your monthly payment by roughly $250–$270. That’s not a rounding error. That’s the difference between a comfortable budget and a stretched one.

Q Does the type of loan I use change the picture?

Significantly. VA loans, for example, require no private mortgage insurance at all — a meaningful structural advantage for eligible veterans and active-duty service members, including the many families connected to Luke Air Force Base here in the West Valley. FHA loans require MIP regardless of down payment. Conventional loans require PMI below 20% down but allow it to be removed once you build sufficient equity. A generic calculator can’t account for which loan type fits your situation, and that single variable can shift your real monthly payment by $150–$300.

Q How does Zillow handle self-employed income?

It doesn’t — and this is where the gap between an online estimate and reality gets the widest. Self-employed borrowers are qualified differently than W-2 employees. Lenders look at net income after deductions, average income over two years of tax returns, and sometimes use bank statement programs that calculate qualifying income in entirely different ways. A self-employed buyer who looks at a Zillow payment estimate has no real way to know whether they’d actually qualify for that loan amount at all — let alone what their real rate and terms would look like. This is one of the most common reasons self-employed buyers get a rude surprise late in the process when they go in without proper guidance from the start.

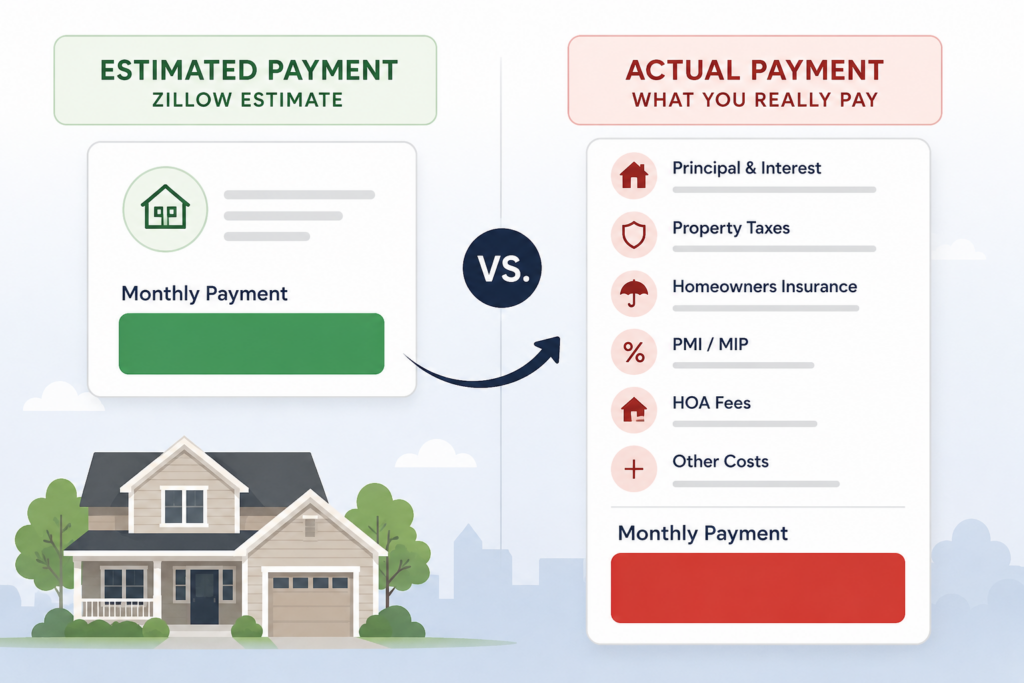

A Real Side-by-Side: Zillow Estimate vs. Actual Payment

Numbers make this easier to see clearly. Here’s a realistic comparison based on a $420,000 home in Peoria, financed with a conventional loan and 5% down — a common scenario for many of my clients. $420,000 Home · 5% Down · Conventional 30-Year Fixed Loan Amount $399,000 Zillow’s Estimated Monthly Payment ~$2,380/mo (generic rate, no PMI, flat tax estimate) Principal & Interest (Actual Quoted Rate) $2,495/mo Private Mortgage Insurance (PMI) +$210/mo Property Taxes (Actual County Record) +$245/mo Homeowners Insurance (Actual Quote) +$165/mo HOA Fee +$85/mo Actual Total Monthly Payment $3,200/mo Gap Between Zillow’s Estimate and Reality $820/month

That’s not a small discrepancy — it’s an $820-per-month gap, or nearly $9,800 a year. For a buyer working with a tight budget, that’s the difference between a home that’s comfortably affordable and one that creates real financial strain within the first year. This is exactly why a generic online number should never be the basis for your home search budget.

Why This Gap Actually Matters

Beyond the obvious budgeting risk, this gap creates real problems during the home search process itself. Buyers who anchor their search around an inaccurate Zillow estimate often end up looking at homes that are actually outside their real comfort zone — and don’t find out until they’re well into the process, sometimes after they’ve fallen in love with a specific house and neighborhood.

It also affects negotiating power. A buyer who walks into an offer with a vague sense of their numbers is in a weaker position than one who has a precise, lender-verified picture of exactly what they can afford and exactly what their payment will be at different price points. For first-time buyers especially, walking in with real numbers — not estimates — changes the entire experience of the search from anxious guesswork to confident decision-making. A Word of Caution

I’ve worked with buyers who fell in love with a home based on a Zillow payment estimate that was $400–$600 below their actual cost. By the time they discovered the real number — sometimes during underwriting, after they were already emotionally invested — it created unnecessary stress and, in a few cases, forced them to walk away from a deal they’d already committed time and money toward. Getting accurate numbers upfront prevents this entirely.

How to Get a Real Number Instead of an Estimate

The fix here isn’t complicated — it just requires going to the right source. Here’s what an accurate payment calculation actually requires:A real rate quote based on your actual credit profile. Not a generic average — your specific score, your specific loan amount, your specific down payment. The actual current property tax bill for the specific parcel you’re considering — pulled from the county assessor, not estimated from a statewide average. An actual homeowners insurance quote for that specific property, accounting for its age, construction, and location-specific risk factors. Correct PMI or MIP calculation based on your actual loan type, down payment, and credit score — not a flat placeholder percentage. Current HOA dues verified directly with the community’s management company, not pulled from outdated listing data. The right loan program for your situation — conventional, FHA, VA, or a self-employed-friendly program — since the program itself changes nearly every variable in the calculation.

This is, frankly, the entire value of working with a real mortgage broker instead of relying on a listing site’s built-in calculator. As a local mortgage broker here in Peoria, I pull these numbers directly — actual rate sheets from multiple lenders, actual county tax records, actual insurance quotes — and give you a number you can genuinely build a home search around. It takes about 15–20 minutes, and it’s free. The Broker Advantage

Because I work with multiple lenders rather than a single institution, I can also show you how the same home would be financed differently across loan programs — conventional vs. FHA vs. VA — so you can see the real payment difference side by side, not just a single generic estimate. That’s a level of detail no online calculator can replicate.

Get Your Real Number — Not an Estimate

Send me the listing you’re looking at, or just give me a call. I’ll pull the actual tax record, run real rate scenarios based on your credit profile, and show you exactly what your payment would be — no generic placeholders, no guesswork.(480) 239-7766 — Call JoeMeet Joe →

A Few More Questions Worth Asking

Q- If I’m buying near Luke Air Force Base, does that change anything?

It can, in a good way. Many buyers near Luke Air Force Base are eligible for VA loans, which eliminate the mortgage insurance line item entirely and typically offer some of the most competitive rates available. If you’re active duty, a veteran, or a qualifying spouse, this single factor can make your real payment significantly lower than a Zillow estimate built around conventional financing assumptions — the opposite direction of most of the surprises in this article, and worth confirming early.

Q- Can PMI ever go away, or is it permanent?

On a conventional loan, PMI can be removed once you reach roughly 80% loan-to-value based on the home’s original value — either through paying down the loan over time or through appreciation, in some cases with a new appraisal. On FHA loans, MIP removal depends on your down payment: 10%+ down allows removal after 11 years, while less than 10% down means MIP stays for the life of the loan unless you refinance into a conventional mortgage later. This is exactly the kind of detail a generic calculator skips entirely.

Q- Should I just trust my Realtor’s estimate instead?

Realtors are excellent at many things, but calculating an accurate mortgage payment usually isn’t one of them — it’s simply not their area of expertise, and most are working from the same generic online tools as everyone else. The accurate number comes from someone actively pulling current rates, your specific credit profile, and the property’s actual tax and insurance figures. That’s a lender or broker’s job, not a Realtor’s.

Before You Fall in Love With a House, Get the Real Number

I’m a local mortgage broker based right here in Peoria, and I’ve helped hundreds of West Valley buyers cut through exactly this kind of confusion. Whether you’re a first-time buyer, self-employed, a veteran near Luke Air Force Base, or just want to know what you can actually afford — let’s talk numbers, not estimates.(480) 239-7766 — Call or Text JoeAbout Joe Hansen →

Helpful Resources

- About Joe Hansen — Mortgage Broker, Peoria AZ

- First-Time Home Buyer Guide — Peoria, AZ (2026)

- VA Loans Near Luke Air Force Base

- Self-Employed Mortgage Loans in Peoria, AZ

- CFPB — Explore Mortgage Rate Tools

- HUD — Understanding FHA Mortgage Insurance

Joe Hansen Mortgage Loan Officer · NMLS# 217716 · AZ LO0911403

Joe Hansen is a licensed mortgage loan officer and broker at Precision Mortgage in Peoria, AZ with over 20 years of experience helping Arizona homebuyers get accurate, honest numbers before they fall in love with a house. He specializes in conventional, FHA, VA, self-employed, and first-time buyer financing across Peoria, Glendale, Surprise, Phoenix, and the greater West Valley.joehansenmortgage.com(480) 239-7766Meet Joe