Native American Home Loans in Arizona: The HUD Section 184 Program Explained

HUD Section 184 Home Loan

A powerful — and often overlooked — federal loan program designed specifically for American Indian and Alaska Native families. Low down payment, no monthly mortgage insurance, and available statewide in Arizona.

What Is the HUD Section 184 Loan?

The HUD Section 184 Indian Home Loan Guarantee Program is a federally backed mortgage program created in 1992 by the U.S. Department of Housing and Urban Development specifically for American Indian and Alaska Native families. It was designed to address a historic problem: because much of Native land is held in federal trust and cannot be mortgaged in the traditional sense, private lenders were reluctant to offer home loans to tribal members — even those who were creditworthy.

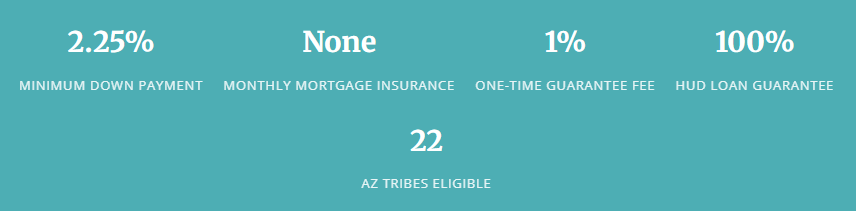

Section 184 solves this by having HUD guarantee 100% of each loan, giving lenders the security they need to serve Native communities. The result is a loan program with some of the most borrower-friendly terms available anywhere — and it’s available right here in Arizona for all 22 federally recognized tribes.

Arizona is fully eligible. Unlike some states where Section 184 loans are only available in select counties, the program is available in every county in Arizona — both on and off Native lands. You don’t have to live on a reservation to qualify.

Key Benefits of the Section 184 Loan

This program stands out from conventional loans, FHA loans, and even VA loans in several important ways:

Low Down Payment

As low as 2.25% for loans above $50,000, or just 1.25% for loans under $50,000 — far less than most conventional loan options.

No Monthly MIP

Unlike FHA loans, Section 184 has no ongoing monthly mortgage insurance premium. This keeps your monthly payment lower for the life of the loan.

No Credit Score Minimum

The program has no stated minimum credit score — underwriting is done manually with a hands-on, common-sense approach rather than automated scoring.

Low Guarantee Fee

A one-time 1% upfront guarantee fee at closing — and it can be financed into the loan. Effective July 2023, there is no annual renewal fee at all.

Flexible Use

Buy, build, rehab, or refinance a 1–4 unit primary residence — on or off Native lands. On-reservation purchases on tribal trust land are also eligible.

Predatory Lending Protection

HUD monitors all fees lenders can charge Section 184 borrowers, providing an extra layer of protection that conventional programs don’t offer.

Stack your benefits: Section 184 can be combined with down payment assistance grants, closing cost assistance, or other subordinate second mortgage programs offered through Arizona state housing agencies or tribal housing authorities — potentially getting you into a home with very little out of pocket.

Who Qualifies for a Section 184 Loan?

Eligibility for Section 184 is tied to tribal membership, not income. Here are the key qualifying criteria:

| Requirement | Details |

|---|---|

| Tribal Membership | Must be an enrolled member of a federally recognized tribe. Verification (Tribal Membership or Citizen Card) is required at application. |

| Primary Residence | The home must be your primary residence — not a second home, vacation property, or investment property. |

| Property Type | Single-family homes, 1–4 unit properties. No condos or commercial buildings. |

| Loan Type | Fixed-rate only (up to 30 years). Adjustable-rate mortgages (ARMs) are not permitted. |

| Debt-to-Income | Maximum back-end DTI of 41%. Manual underwriting — strong payment history is important even without a score requirement. |

| Location | Property must be in an eligible area. All counties in Arizona qualify — both on and off tribal land. |

| First-Time Buyer? | Not required. Both first-time and repeat homebuyers are eligible. |

Important note on credit: While there is no stated minimum credit score, the program does use manual underwriting and closely reviews the quality of your credit history. Collections, recent derogatory marks, and unpaid judgments can still be an obstacle. This is why working with an experienced loan officer who knows the Section 184 guidelines is essential.

Arizona’s 22 Federally Recognized Tribes

All 22 federally recognized tribes in Arizona have members who may be eligible for the Section 184 program. The Section 184 loan is available statewide in Arizona — meaning tribal members can use this program to purchase a home anywhere in the state, not just on reservation land. Ak-Chin Indian Community, Cocopah Indian Tribe, Colorado River Indian Tribes, Fort McDowell Yavapai Nation Fort Mojave Indian Tribe, Fort Yuma Quechan Tribe, Gila River Indian Community, Havasupai Tribe, Hopi Tribe, Hualapai Tribe, Kaibab Band of Paiute IndiansNavajo NationPascua Yaqui Tribe, Pueblo of Zuni, Salt River Pima-Maricopa Community, San Carlos Apache Tribe, San Juan Southern Paiute Tribe, Tohono O’odham Nation, Tonto Apache TribeWhite Mountain Apache Tribe, Yavapai-Apache Tribe, Yavapai-Prescott Indian Tribe

Source: Arizona State Museum – Federally Recognized Native Nations in Arizona

On-Reservation vs. Off-Reservation Purchases

One of the most misunderstood aspects of Section 184 is that it works both on and off reservation lands. Here’s how the two scenarios differ:

Purchasing a Home Off Tribal Land (Most Common)

If you’re buying a home in the Phoenix metro, Peoria, Scottsdale, Mesa, or anywhere else in Arizona off reservation, the process works similarly to a standard FHA loan — but with better terms. You’ll work with an approved Section 184 lender (like Precision Mortgage), and the loan process is streamlined.

Purchasing a Home on Tribal Trust Land

Buying on tribal trust land involves additional steps. Because the land itself is held in trust and cannot be mortgaged, the buyer works with their tribe and the Bureau of Indian Affairs (BIA) to establish a leasehold estate — a 50-year lease of the land. The home and the lease are what is mortgaged, not the land itself. Both HUD and BIA must approve the process. This takes more time but is absolutely doable with the right guidance.

Trust land purchases require an experienced lender. Not every lender knows how to navigate trust land transactions. If you’re looking at an on-reservation purchase in Arizona, contact Joe Hansen directly to make sure your loan is structured correctly from day one.

How to Apply for a Section 184 Loan in Arizona

The application process is straightforward when you work with an experienced Section 184 lender. Here’s what to expect:

- 1. Verify Your Tribal Enrollment. Contact your tribe directly to obtain proof of enrollment (a Tribal Membership Card or Citizen Card). Neither your lender nor HUD can assist with this step — your tribe manages enrollment.

- 2. Connect with a HUD-Approved Section 184 Lender. Not all lenders are approved for Section 184. Joe Hansen at Precision Mortgage can walk you through eligibility, expected loan amounts, and all program requirements with no cost or obligation.

- 3. Consider a Homebuyer Education Course. While not mandatory, HUD-approved homebuyer counseling is recommended — and some tribes and lenders may even offer financial assistance for completing it. It helps set you up for long-term success.

- 4. Complete Your Loan Application. Your lender will review your income, debt-to-income ratio, credit history, and the property you intend to purchase. Remember — manual underwriting means your full story matters, not just your score.

- 5. Close and Move In. At closing, you’ll pay the 1% upfront guarantee fee (which can be rolled into the loan). After that, no monthly mortgage insurance, ever. Welcome home.

Frequently Asked Questions

Can I use Section 184 if I don’t live on a reservation?

Yes. The program is available to enrolled tribal members purchasing a home anywhere in Arizona — on or off tribal land. Many Section 184 borrowers are buying homes in Phoenix, Tempe, Mesa, Peoria, and across the Valley.

Is there an income limit to qualify?

No. Unlike some assistance programs, Section 184 has no borrower income limits. Eligibility is based on tribal membership, creditworthiness, and ability to repay the loan.

Can I refinance with Section 184?

Yes. Section 184 can be used for rate-and-term refinances. However, cash-out refinancing options are subject to stricter documentation and lender-specific guidelines, so ask your loan officer about your specific situation.

What’s the difference between Section 184 and FHA?

Both are government-backed programs with low down payments, but Section 184 is exclusively for enrolled tribal members and offers several advantages: no monthly mortgage insurance, a lower one-time guarantee fee (1% vs. FHA’s 1.75%), and manual underwriting that considers your full credit picture. For eligible borrowers, Section 184 is almost always the better option.

Does the property have to be new construction?

No. Section 184 can be used to purchase an existing home, build a new home, or rehabilitate a property in need of repairs. It’s a flexible program covering most primary residence purchase and improvement scenarios.

How long does the Section 184 process take?

Off-reservation purchases in Arizona typically follow a standard timeline similar to FHA. On-reservation trust land purchases take longer due to BIA approval requirements — plan for additional weeks in that scenario. Choosing an experienced lender who knows the process makes a significant difference.

For more information, reach out to Joe Hansen for all your HUD 184 Native American Loan options and questions. Go here to compare the FHA loan options.

Official Resources & Helpful Links

- HUD Section 184 Program Overview – hud.gov

- HUD Section 184 Borrower Resources – hud.gov

- HUD Approved Section 184 Lenders List – hud.gov

- Arizona’s 22 Federally Recognized Native Nations – AZ State Museum

- AZ Dept. of Education – Tribal Contacts

- joehansenmortgage.com – Talk to Joe Hansen Directly

About the Author

Joe Hansen | Joe Mortgage

Joe Hansen is a licensed Mortgage Loan Officer at Precision Mortgage in Peoria, Arizona (NMLS# 217716 · AZ LO0911403). He serves the greater Phoenix metro area and specializes in helping borrowers find the right loan — including specialty programs like Section 184. “Your home. My mission. Let’s make it happen.”